How AI and Data Quality checks enable insurers to thrive amid global adversity

The insurance sector in Europe and the Americas continues to boom and remains solid. The Mapfre Economics Research Department forecasts that the insurance business will continue to grow above the trend of recent years. Despite facing difficult times, the war between Ukraine and Russia, the increase in inflation, and the still present consequences derived from the pandemic.

The outlook appears to be positive. According to the Insurance Information Institute, the weight of the insurance sector will reach 3.1% of the worldwide gross domestic product (GDP) in 2020, and statistics indicate that it will continue to grow. While these results are favorable, this market is facing a transformation process due to regulations and technology known as Big Data. The previous global events and the inevitable generational change push this industry to implement digitalization in its operations and offer the public a competent and cutting-edge service.

Insurance companies handle international information of all kinds in scope, thus needing to turn to storage platforms, such as the cloud, to back up data from their central systems to achieve operational efficiency and more significant business agility. The same is true for all the data captured from the involved customers. Employees must make the most of this digital environment to improve the customer experience. This action not only relies on the digital adoption by the company but also on the implementation of appropriate solutions that address the real problems involved in managing massive databases.

This white paper aims to help companies in the field understand how artificial intelligence can overcome the challenges of the new international landscape.

What it takes to keep pace with this new era

As a channel that distributes various insurance products, the bancassurance sector has gone through ups and downs in recent years. In the second quarter of 2018, McKinsey held its Global Bancassurance Forum in Rome, presenting new research and data from a comprehensive benchmarking study conducted by Finalta on a universe of banks with head offices in 27 countries.

“ Overall, the bancassurance industry is recording a marked increase in premiums worldwide. Between 2011 and 2017, the bancassurance channel's growth was faster than that of other channels, both in life insurance and in other categories. ”McKinsey, 2018

Thanks to the above, there is now greater demand in the industry. Insurers have access to more opportunities, which demand that companies adapt to the new digital era. These audiences are pushing the insurance industry to digitalize its processes through AI until companies have been driven to invest more in platforms than human talents, such as call centers. It requires a double effort to say goodbye to analog tools and, at the same time, welcome holistic solutions that consider all the current issues. Adopting these new digital solutions may seem like a complicated and time-consuming task. Still, knowing and understanding the industry's challenges makes it possible to make the digital leap assertively. The following are three of the main challenges to be confronted:

In the middle of the transformation: Digitalization remains a privilege

Violet Chung, McKinsey partner in Hong Kong, shares that technology adoption could have immediate and lasting effects on customer relationships, product innovation, and value chain evolution. Experts confirm the need to migrate from analog tools to digital and integrated solutions. However, the presence of minorities in the landscape, such as rural communities, who do not have access to the Internet, let alone experience digital platforms, is not stressed and is even minimized. The arguments in favor of digital access are clear. Digitalization drives social and financial inclusion. Yet, this action requires governments to provide resources and funding. Insurers do not have a role in this transformation, but they do have a role in benefiting this population despite the digital gap. Even if this is minor, there is an existing market in these communities, which also needs insurance cover, for example, claims, catastrophes, indemnities for closure, work incapacity, theft, vandalism, breakdowns, or loss of benefits.

The challenges this situation creates are clear and present for every insurer. Digital adoption is slowed, especially in the early stages of sales conversion. Data plans and internet devices are not affordable for low-income people in the region, so initial information, preferably presented through emails, must be shared face-to-face. Door-to-door prospecting is still a reality for many companies. This task is even more complicated because there are few opportunities to obtain as much customer data as possible. Insurers spend even more to send trained personnel to these communities, drastically reducing the window of opportunity.

Once the company obtains new records from these communities, the next step is manual data entry, leading to human error. A basic database storage system will never be able to detect duplicates and invalid information quickly. From then on, the follow-up and all efforts will be in vain, especially regarding addresses. Should the customer continue the process and purchase the service, it will only be possible to follow up through traditional correspondence. The previous is standard and common practice in many countries, but the scenario takes a 180-degree turn regarding remote addresses with no numerical system or supervised order. Most addresses have an unlogical and arbitrary order, typical of a small remote community, which operates under its own rules. Far from discussing whether this is correct, it is a reality that affects insurers and makes follow-up processes costly.

If the insurer in question charges for the service, periodic invoices are also sent by correspondence. An undetected data error can lead to significant leakage of money. All data obtained in the databases need to be validated instantly. While this does not ensure total control due to the nature of the scenario, it certainly provides clarity to the insurer's customer portfolio. There will be incorrect records or non-existent addresses, but the insurer will not waste time manually confirming this. Correcting is easier when you know what is wrong, thus saving the agent/insurer time, money and effort.

Finally, on this point, it is crucial to understand that people living in rural communities choose to settle with trustworthy companies. Reputation, whether good or bad, travels quickly from voice to voice. This audience does not have access to digital advertising; if they do, it is limited. Little or no access to the Internet encourages an organic lifestyle. Good data management leads to good tracking and customer service, which leads to a healthy relationship with customers, and in this case, a thriving relationship with an entire community.

Customer retention and success: a data hygiene prioritizing culture

Getting customers is a complicated job, and keeping them loyal over the long-term ranks as one of the most complex tasks for any insurer. The objective of insurance agents of keeping people happy with their agency's collections and profits can be overwhelming. Insurance agencies primarily sell the promise of life and business peace of mind to their customers in health, property, auto, and business policies. Given the importance of financial protection for life's unforeseen events, and in the context of their country, getting policyholders is not that difficult, but keeping them satisfied is.

The truth is that there are a series of behaviors, procedures, and responses that push the insured to abandon their insurance agency. Insurance agents lose customers, and the failure to retain them creates a knock-on effect for the entire company. It is an error to think that AI replaces human talent. Both scenarios are complementary.

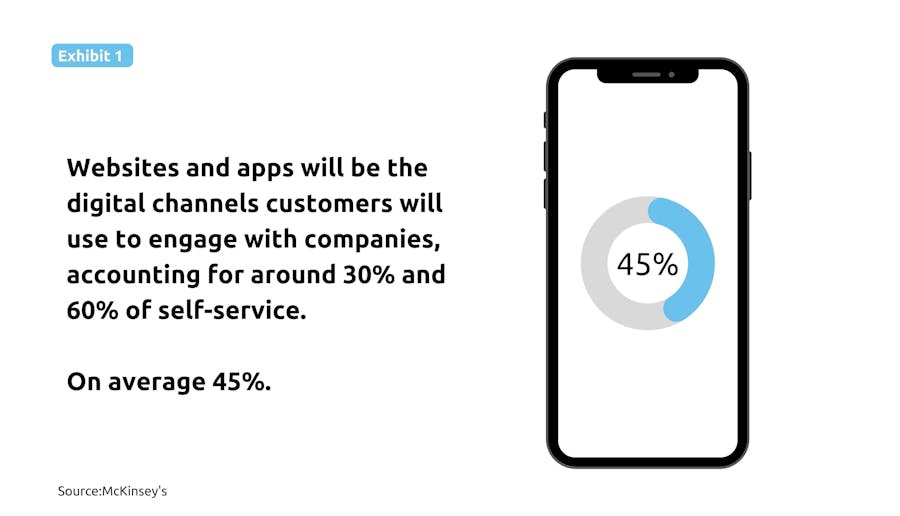

According to McKinsey's analysis, websites and apps will be the digital channels customers will use to engage with companies, accounting for around 30% and 60% of self-service (Exhibit 1): "A true omnichannel world will emerge: when customers interact with a company, they will have access to a wide range of contact options, from social media and chat to voice."

The most effective way to avoid making the same mistakes is to be aware of the previous events. Listening to complaints from dissatisfied customers is the easiest way to detect which processes need to be updated or replaced. Digitalization represents a solution to all problems, both the communication channel from customer to insurer and from insurer to customer. It is now crucial to innovate savings formulas in the process. Hybrid products will play a vital role in the coming years. Companies must offer products and services that mostly fit inside cell phone screens and leave the organic approach for a well-justified and timely follow-up.

Now that it is clear why it is vital to digitalize processes, it is time to talk about customer behavior towards these venues: from customer to insurer. There is a growing trend towards hyper-customization of insurance products that responds to an expectation of flexibility on the part of the customer in the configuration of the product. For example, being able to activate/deactivate the insurance and adapt the sum insured and the coverages fast. Another great benefit is offering customers a handy reference space. For example, they will need to check their insurance status and coverage if they travel. In a matter of clicks, they can obtain all this information without waiting in long lines, either in person or over the phone.

Modular products that allow complementary services to be added immediately to the value proposition made to the customer are also gaining importance. In this case, having a holistic database management solution solves two issues. The first is to offer the customers the option to change their insurance or to consult it without contacting an agent, so they can act whenever needed. The second is to provide the service that the customers specifically request and thus avoid disturbing them with more products or services they are not interested in. This system allows customers to breathe and enjoy their personal space.

Another reason customers leave their insurers is related to the communication from insurer to customer. These perceive that the agent involved is only after the sale and not taking care of the relationship. The aim is to offer an automated, humanized platform open to dialogue without discarding organic contact. Customers need to know that they will receive excellent and prompt attention. After closing the deal, sending a message with basic information and setting up an open platform is not enough. It is a mistake to assume that the customer will always contact the insurer if they have a problem or a question. Communication must be permanent, and the information sent must be systematic and updated. The insurer avoids dissatisfaction by being the first to contact the customer at the right time. If the customer has an issue, they will also need a platform to ask for assistance, but it should not replace the agent entirely. Many clients are unaware of their status until they receive help.

In addition to basic services, insurance companies can think outside the box. It is advisable to send corporate greetings during the months of national holidays, birthdays, and national events. The premise: Use AI to offer a humanized service. To accomplish this is essential to have a trustworthy database to flow follow-up campaigns, managing accurate information. The data obtained through an AI solution from customers can even reflect the lifestyle of the person in question, whether they are an athlete, a student, a traveler, or a family member, among others. From this information, the company can have a better understanding of the customer, therefore, predict their behavior and thus make the follow-up more efficient. What insurance or extensions to offer, and when to provide them? Data will talk.

Security and compliance: Promoting a trustworthy space

End users will only build lasting relationships with insurers they can fully trust. To keep these users happy and reduce costs simultaneously, companies need to improve how they drive their digital service transformations forward. Insurers are starting to see the benefit of a security and compliance approach that accelerates their digital transformations and improves the bottom line.

Despite market saturation and the predictive industry proposition, today's insurers (and payment industry) find differentiating potential in digital adoption through their payment and transaction platforms. This point becomes even more critical if an adoption prioritizes transparency, a secure space in which user data is protected and used only for previously agreed on purposes.

Regardless of the ethics of the company and its agreed terms and conditions, agents need tools that can provide clarity in the processes. It is common for insurers to opt for segmented digital applications, which in most cases do not speak the same language, thus wasting and biasing highly relevant data and even missing opportunities by losing focus on security. When digitalizing processes, it is of vital importance for insurers to acquire solutions that can be trusted to convey confidence to their end customers. Duplicate, incomplete, biased, and poorly validated data lead to errors. If that same data migrates from application to application to perform a single task, in addition to wasting time in the process, the company is working with unusable and vulnerable data.

Less is also more in this context. Working with integrated platforms in a single space allows insurers to track every movement in their databases meticulously. It is not only a matter of having personal customer data but also of keeping an automated record of customer actions, as well as the location, date, time, account details, and all the information required to provide a secure platform.

Humanizing the end-to-end experience

The insurance industry has a unique peculiarity: it has been selling the same product for centuries. This could lead one to conclude that it is a stagnant industry. However, it is quite the opposite. Many things are changing in the insurance industry worldwide. The digital era has transformed the industry. It now has access to multiple channels with which it can capture millions of records internationally. This openness is undoubtedly beneficial for business. Yet, it gives rise to a new problem: Agent and AI pairing problems.

With the data obtained from multiple sources, there is a risk of fragmenting information. Insurers collect multiple inputs more than any other industry. Opportunities are created digitally and through agents. At this level, there is a challenge for the agent to standardize a database. Having only manual and semi-automatic tools limits the agent's performance, which generates dissatisfaction at the client level and employee one. The limited adoption of digital and up-to-date work tools results in the employees of an organization, in this case, insurance agents, failing to meet customer expectations. As a result, there is only room for disposable relationships. The agent spends more time-solving problems, which AI can quickly solve. In this scenario, employees' efforts are misdirected, and sooner rather than later, they lose motivation and interest in proposing new business models, opting to maintain a constant but mediocre workflow.

The agents who have the task of visiting customers door to door need an efficient database with which they can obtain addresses, names, insurance purchased, and the previous follow-up job, even if another agent has done this. The most common mistake when performing this activity is visiting customers who have already been recent. This human error affects the insurer's credibility and the relationship between agent and customer, hindering the growth of the opportunity.

It is essential to understand that the team behind the account is not a group of robots. They are people with feelings, dreams, and concerns. When they feel they do not represent value to the organization, they lose interest in fulfilling their functions. Fatigue from long hours and work overload are other factors that lead workers to worry a little more about their well-being than anything else. When insurers invest in the offer but not the work tools, they make it clear that the priority is the sale and not the person who made it possible.

Human talent needs attention. When the latter chooses to resign, the insurer has to invest time, money, and effort in training the newly hired talent. The company's performance slows down. The success of the company is also affected. Here it becomes clear that a company's success is linked to customer service and the support that employees receive.

The insurer must provide a broad view of the business to retain employees. For agents to perform a great job, digital adoption is required, opting for integrated solutions that facilitate follow-up and customer service. Insurance agents need to see the added value that the company offers. This action will prevent them from migrating to other insurers or pursuing commissions through more realistic goals.

Clean data: a solution to all issues

The world events made it possible to expose one of the most significant weaknesses of the insurance industry: its digital and technological capabilities. Insurers are still working with their rudimentary system, which translates into using many forms to complete, phone calls, among others.

The insurance industry's resistance to implementing digital technologies is marked. As insurers see an increase in digital adoption in other companies, they know they are not only at risk of being left behind, but they could also become obsolete with other companies offering insurance as an added service. Technology adoption will inevitably make some companies more competitive, leading to a redefinition of the competitive landscape. While obtaining data through the Internet and digital services is becoming easier, on the other hand, it is increasingly difficult for companies to have proper control of massive data, which directly harms customer relationships.

It is not enough to digitalize processes. It is a priority for insurers to operate with native and holistic solutions. Agents must work with monitored databases with validated information and free from duplicate records. AI is required to manage a large volume of data. Wasting valuable time manipulating bulk data is no longer an option. Agents take too long to find fragmented lead data, and contact data such as email, phone numbers, and addresses are invalid. Holistic solutions enable end users, managers, and developers to focus on new business model propositions, acquire new opportunities, and strengthen customer relationships.

By making the digital leap and taking advantage of the booming Big Data era, the insurance company is empowered to make decisions based on data rather than opinions, benefiting the company and its multiple levels. Insurers no longer need to question whether they will implement digital processes in their companies. Instead, they will ask themselves if they are ready for success.